You may qualify for incremental tax benefits!

On July 4, 2025, new legislation was signed into law that included multiple favorable depreciation

changes for businesses associated with the Section 179 Allowance and Bonus Depreciation. These

changes permit businesses to potentially deduct the cost of qualifying property in the year placed in

service, rather than taking the deductions over the tax life of the asset. This may result in an

acceleration of tax benefits.

To make the most of the new benefits, it's critical to begin planning immediately to secure

equipment availability.

Click to our List of Equipment for Sale

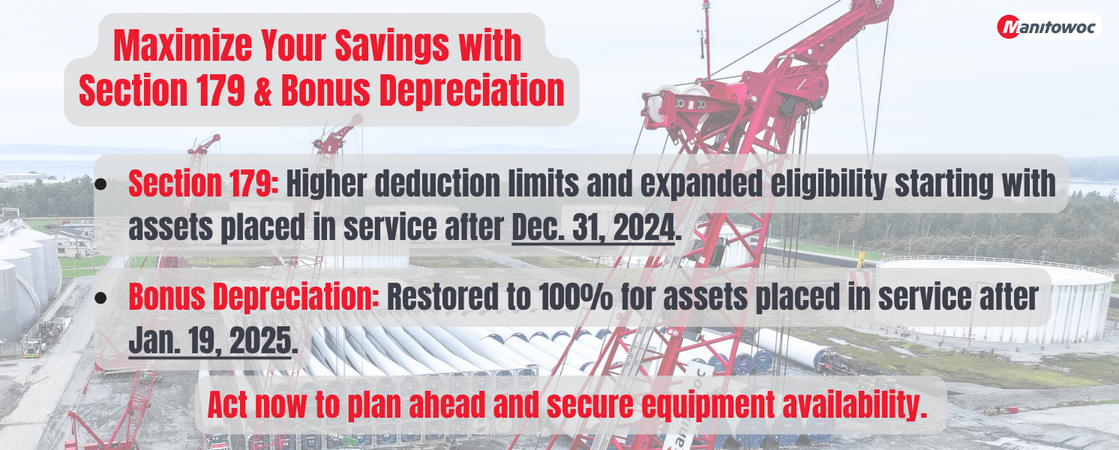

Section 179 Allowance

Section 179 allows eligible taxpayers to deduct the cost of qualifying property up to an annual limitation

in the year placed in service. The Act increased the annual limitation and modified eligibility

requirements so more taxpayers will qualify to take Section 179 deductions for property placed in

service in taxable years ending after December 31, 2024.

Bonus Depreciation

Bonus depreciation allows businesses to deduct a set percentage of the cost of qualifying property in

the year placed in service. Any remaining cost is deductible over the tax life of the property. The Act

increased the bonus depreciation percentage to 100% for assets placed in service after

January 19, 2025.

Contact your accountant or financial advisor today to fully understand how the new tax laws could

benefit you when acquiring new equipment, to ensure the equipment and the associated financial product

qualifies for favorable tax treatment.

The above contains general information only and is not intended to be tax advice. It is not a substitute for

such professional advice or services, nor should it be used as a basis for any decision or action that may

affect your business. Before making any decision or taking any action that may affect your business, you

should consult a qualified professional adviser.

Contact Shawmut Equipment about our available cranes and equipment.

- Log in to post comments